here is a good recap (Part II) of GSE story

investment in GSE common’s strategy

- preferred

- sell once start recap? do I need to wait for them to convert to common? or do I need to hold them for longer term?

- Once reach 50%, sell some amount to make sure I do not lose the original investments?

- common stock

- buy common before recap (now) and sell them soon (and/or) buy put after re-ipo (relisting) because of the reference price history of AIG

- right before or after completion of IPO, buy call of common

Should I buy OTC options?Options trading | Options liquidity and trading solutions | GAIN Capital or this one Best Options Brokers for OTC Options. I have called Etrade and Gain Capital customer service, they do not offer OTC options.

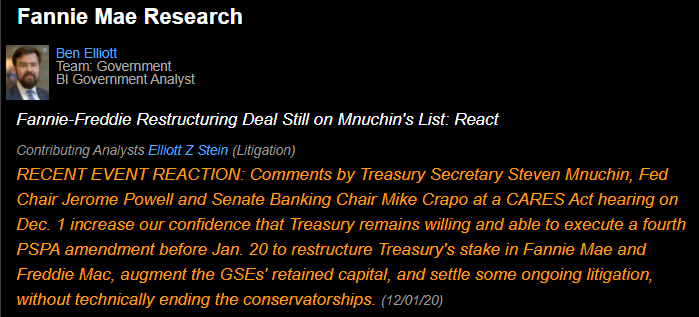

- 12/01/2020 – hearing from banking committee. Crapo

https://www.banking.senate.gov/hearings/11/20/2020/the-quarterly-cares-act-report-to-congress

HoldenWalker99 @HoldenWalker99·

.@MikeCrapo opening statement comments to @USTreasury @stevenmnuchin1 are very significant in the face of recent lobbying efforts to undermine GSE reform. Chances of PSPA amendment increasing.

Every GSE reform naysayer wants @FHFA and @USTreasury to stall administrative action and wait for Congress to pass legislation. Well, Congress (via Senate majority party chair of Senate Banking) just said to go ahead with administrative action.

- 11/30/2020 – Ackman said commons can go to $10 quickly, is he right or just to promote his position?

Bill Ackman’s top share tip for 2021

- Dec 10 supreme court might be one catalyst for commons

- Treasury wants to finish the job before next admin

- Even Biden admin might continue with the privatization

- 11/29/2020 – listen to this if I can get it for free

THE ULTIMATE ELECTION TRADE: FANNIE AND FREDDIE – LIVE WITH GABRIELLA HEFFESSE

- 11/24/2020 – Michael Bright continues to attack release of GSE

Wall Street Warns Mnuchin Against ‘Hastily’ Ending the GSE Conservatorships pmu…@imfpubs.com

After hearing the rumors that the Federal Housing Finance Agency wants to expedite ending the GSE conservatorships before President Trump leaves office, Wall Street has a message for the Treasury Secretary: Don’t do it.

At least that’s what the Structured Finance Association suggested in new correspondence to Treasury chief Steven Mnuchin.

“SFA reiterates our support for the ultimate goal of releasing the GSEs from conservatorship and to increase the role of private capital in our nation’s housing finance system in a responsible manner,” writes SFA CEO Michael Bright.

The former Ginnie Mae interim president said the Wall Street trade group applauds Treasury’s work putting Fannie Mae and Freddie Mac on sound financial footing, but warned a “hastily thrown together exit from conservatorship based on the political calendar risks undoing the positive work that has been accomplished and is currently underway.”

SFA, which represents almost 400 institutional members, wants Treasury – the holder of Fannie/Freddie senior preferred shares – to “chart a course that will allow a responsible transition for the GSEs…”

- 11/23/2020 – it is coming, BUT Biden admin might not like it

Virginia’s Freddie, Fannie regulators seek to end Govt. control before Trump’s exit

Regulators of the Federal Home Loan Mortgage Corporation or Freddie Mac alongside Washington-headquartered mortgage loan company Fannie Mae, had been exploring an option to break free from Govt. control as early as before January 19, when the new US President-elect Joe Biden would swear to take the Oval Office, a Wall Street report published late on Friday had unveiled citing sources familiar with the subject-matter who wished to remained anonymous given the scale of sensitivity of the issue.

On top of that, according to Friday’s Wall Street Journal report, Federal Housing Finance Agency (FHFA) director Mark Calabria, the former chief economist for Vice President Mike Pence, had stepped up his efforts over the recent past to return the Government-sponsored entities into the private market, nonetheless, an accomplishment of a process of such magnitude before January 20 would be a far cry, suggested industry experts.

Besides, followed reveal of the Wall Street Journal report, several policy experts were quoted saying that the President-elect Joe Biden, who had vowed to proffer affordable housing solutions during his electoral campaign, would more likely to ask Calabria to stall his ploys.

- 11/23/2020 – some push back on GSE release

Charles Gasparino @CGasparino BREAKING on @FannieMae

@FreddieMac $FNMA (1 of 2) — Housing and economic aides close to @JoeBiden

are legitimately worried that @MarkCalabria and @stevenmnuchin1 will enact a GSE reform that will be difficult to unwind by new administration. It’s the reason why they are spreading

Charles Gasparino @CGasparino 58m Replying to @CGasparino (2 of 2) that Mnuchin is jeopardizing his legacy at @USTreasury if he does something that screws up the housing market. Story developing $FMCC

- 11/22/2020 – is fourth amendment to the PSPA coming?

Charles Gasparino @CGasparino Nov 22

BREAKING on $FNMA/$FMCC (1 of 4): My sources say the most likely path to GSE reform is a fourth amendment to the PSPA that ends to net worth sweep 100% and sets a milestone path to ending conservatorship. Meanwhile housing interest groups are bombarding

@stevenmnuchin1

w warnings

- 11/20/2020 – It is really a delicate move and takes so long. Is it the end of tunnel?

Fannie, Freddie Overseer Looks to End Federal Control Before Trump Leaves

Long-shot effort could affect cost and availability of mortgages for millions of Americans

The Treasury secretary must agree to any move to alter the terms of either the companies’ bailout agreement or the government’s stakes. One person familiar with the effort said Mr. Mnuchin is supportive of locking in a path to private ownership but mindful of steps that could disrupt the housing-finance market.

Mr. Calabria has met twice recently with Mr. Mnuchin to discuss an expedited exit of the companies from government control, most recently the week of Nov. 9, according to people familiar with the meetings, which also involved Larry Kudlow, the director of the White House’s National Economic Council. Mr. Mnuchin was noncommittal about the push, the people said.

- 11/19/2020 – read this

BankThink Don’t believe doom and gloom on Fannie, Freddie

- 11/18/2020 – a negative view on new FHFA’s new capital rule

Is GSE reform dead on arrival under Biden?

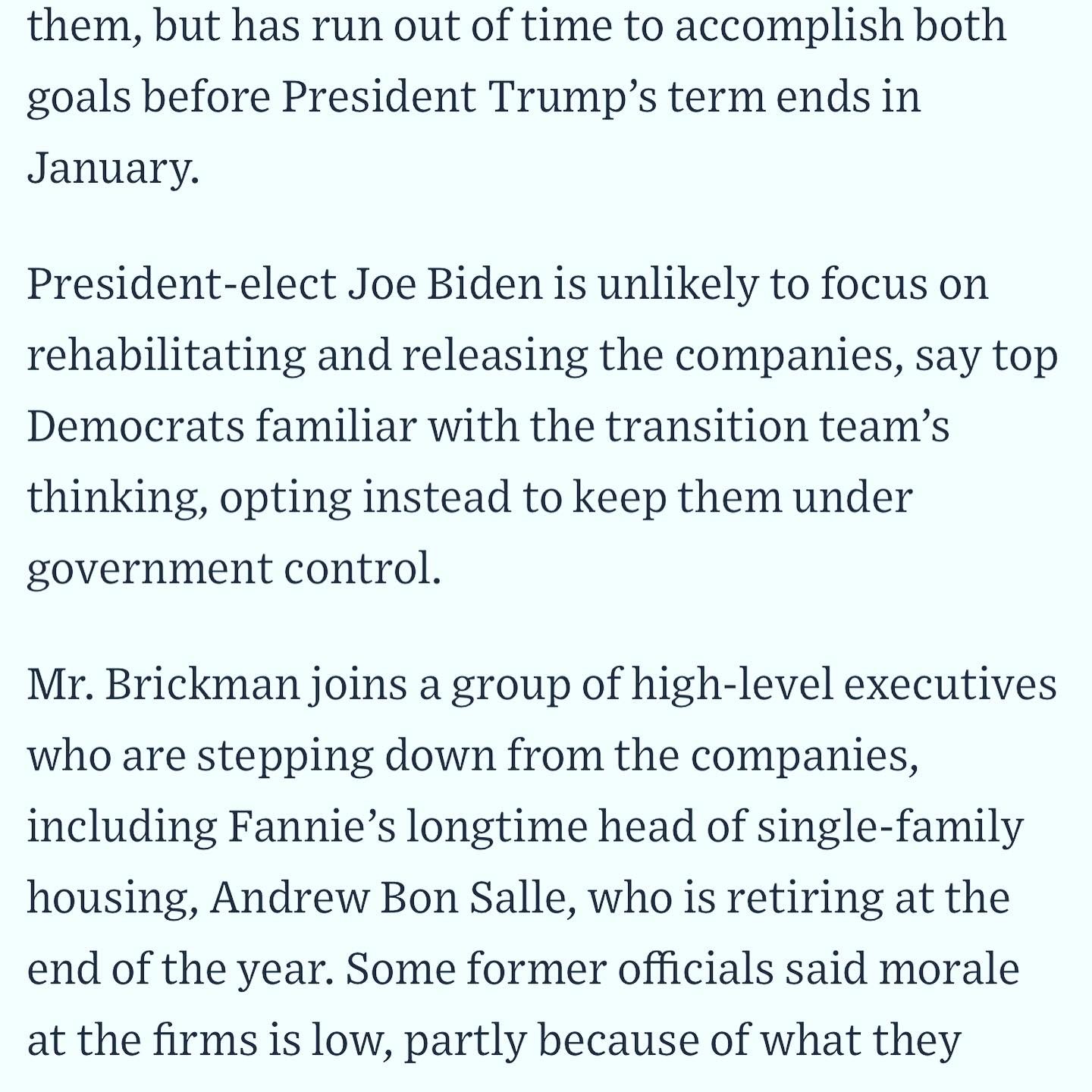

WASHINGTON — The Trump administration in the last two years has laid the groundwork to free mortgage giants Fannie Mae and Freddie Mac from conservatorship without any congressional help. But following President-elect Joe Biden’s victory, mortgage industry veterans predict those efforts will slow considerably or stop altogether.

Some have speculated that the incoming Biden administration may not view reforming the government-sponsored enterprises with the same urgency as President Trump’s appointees, and could view the status quo — the two companies remaining in conservatorship — as sufficient for the moment.

- 11/18/2020 – final capital rule just comes. PSPA Amendment next on the agenda, maybe the end of this year.

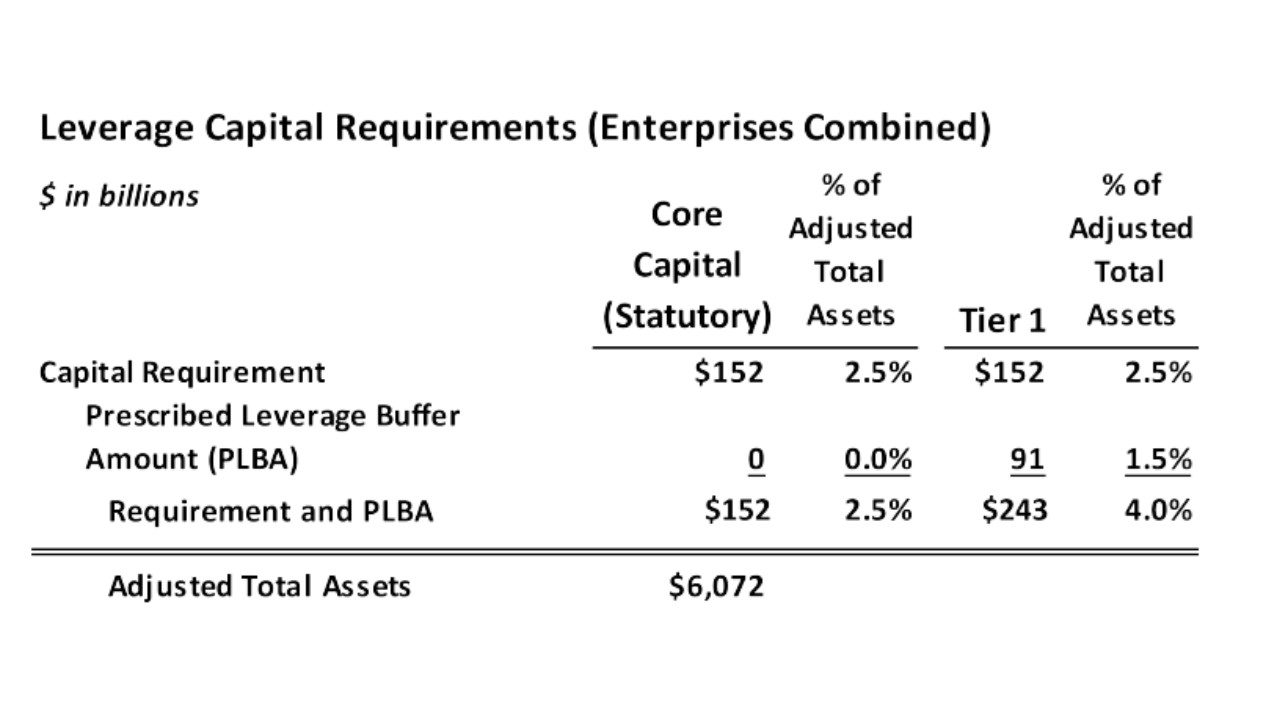

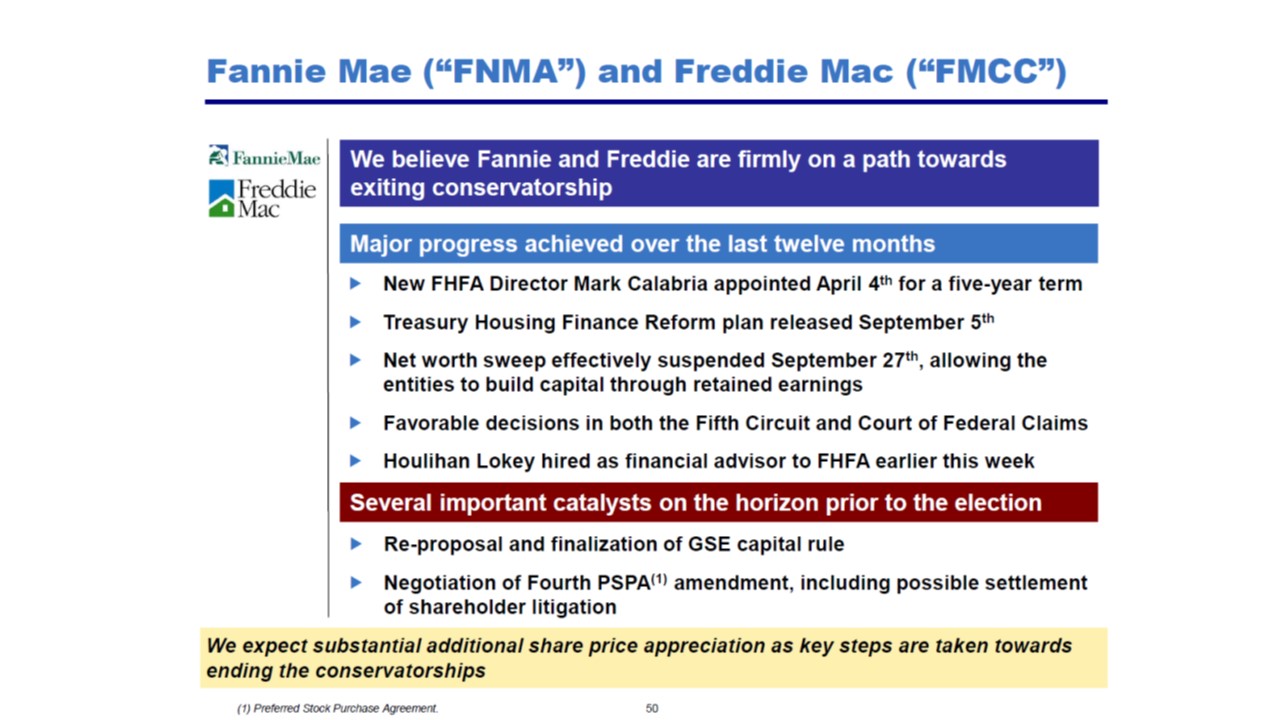

FHFA issues Final Capital Rule for Fannie Mae, Freddie Mac

GSEs to maintain tier 1 capital in excess of 4%

page 22 of the pdf report

The Federal Housing Finance Agency (FHFA) released its Final Capital Rule Wednesday for mortgage giants Fannie Mae and Freddie Mac as it continues to work toward ending conservatorship.

The final rule mandates that the GSEs maintain tier 1 capital in excess of 4% to avoid restrictions on capital distributions and discretionary bonuses.

For example, as of June 30, 2020, the enterprises together would have been required to maintain $207 billion in common equity tier 1 capital, $265 billion in tier 1 capital, and $283 billion in adjusted total capital. For each enterprise, as of June 30, 2020, the adjusted total capital required under the buffer-adjusted risk-based capital requirement would exceed the tier 1 capital required under the buffer-adjusted leverage ratio requirement.

The FHFA explained that the increase in required amounts of regulatory capital, relative to the proposed rule, is due in part to the increase in the enterprises’ adjusted total assets to $6.6 trillion, a 9% increase from the enterprises’ $6.1 trillion in adjusted total assets as of September 30, 2019.

“Fannie Mae and Freddie Mac have a mission to serve the American housing market during good times and bad,” FHFA Director Mark Calabria said. “After considering all the comments on the proposed rule, and the Financial Stability Oversight Council’s review of the secondary mortgage market, FHFA is confident that the final rule puts Fannie Mae and Freddie Mac on a path toward a sound capital footing.

“Increased capital means that they can serve all Americans, especially low- and moderate-income families, throughout the economic cycle,” Calabria said. “The final rule is another milestone necessary for responsibly ending the conservatorships.”

The FHFA issued the final rule after reviewing all 128 comments on its proposed rule, along with hosting two webinars and listening sessions, which it says fulfills Congress’ Housing Economic Recovery Act of 2008 mandate to establish risk-based capital requirements for the government-sponsored enterprises.

Other key changes from the proposed rule include:

—Increased capital relief for credit risk transfers

—Reduced capital requirements for single-family mortgage exposures subject to COVID-19 related forbearance

—Increased the exposure level risk-weight floor for single-family and multifamily mortgage exposures to 20%

Previously, Fannie Mae and Freddie Mac said the proposed capital rule would mean they might have to raise the guarantee fees they charge to package home loans into securities that are sold to bond investors.

Hannah Lang @hannahdlang Replying to @hannahdlang

Per FHFA officials, the move to finalize the capital requirement tees up FHFA and Treasury making amendments to the PSPAs to end the net worth sweep sometime before the end of this year, which would allow the GSEs to retain all of their earnings. (Current cap is $45 bil)

Fannie-Freddie Watchdog Demands Capital Above $280 Billion

By Joe Light

November 18, 2020, 1:00 PM PST Updated on November 18, 2020, 2:56 PM PST

Fannie and Freddie shareholders also hope an amendment to the bailout agreements will somehow reduce the government’s massive ownership stake in Fannie and Freddie. In addition to warrants to acquire nearly 80% of the companies’ common stock, the government owns more than $200 billion in “senior” preferred stock that could be an impediment to future public offerings.

Because the Biden administration is unlikely to share the goal of releasing the companies in the near term, Calabria has sought to strike a last-minute amendment with outgoing Treasury Secretary Steven Mnuchin. It’s not yet clear whether Mnuchin will prioritize finalizing such a complicated agreement in the two months he has left in office.

- 11/18/2020 – good hire of FNMA? ready to exit conservatorship? Even though Bair had long been a critic of the structure of Fannie and its brother Freddie Mac

Former FDIC head Sheila Bair to chair Fannie Mae board

Sheila Bair, the former head of the Federal Deposit Insurance Corp. during the 2008 financial crisis, will chair the board of the government-controlled mortgage giant Fannie Mae beginning Nov. 20, the company announced Wednesday.

Bair joined Fannie’s board in August 2019. Her fellow directors unanimously elected her the successor to Jonathan Plutzik as chair, though Plutzik will remain on the board. The selection comes as Fannie — under the guidance of its regulator, the Federal Housing Finance Agency — is attempting to exit conservatorship, where it has lingered since its bailout in 2008.

Bair had long been a critic of the structure of Fannie and its brother Freddie Mac going back to her role in the George W. Bush administration. While she has acknowledged the important role the two government-sponsored enterprises play in buying mortgages and selling them in securities to investors with an implied government guarantee, she has pushed for Congress to decide their permanent fate.

“Our future financial stability demands that we deal with these implicit liabilities head on, and limit the ability of private companies to take risks at the expense of the taxpayer,” Bair said in a 2010 speech as the chair of the FDIC. “In the case of the mortgage GSEs, there are a variety of options for making some of their functions governmental while putting others in private hands. But what we cannot do is perpetuate their quasi-governmental status, which privatizes gains and socializes losses.”

Fannie Mae has paid $181.4 billion in dividends to the Treasury Department after drawing $119.8 billion in bailouts as of Sept. 30, according to the company’s latest financial results. After years of stalled legislation to reform Fannie and Freddie, the FHFA and the Treasury announced a suspension of the dividend payments while the companies are allowed to rebuild their capital reserves in preparation for exiting conservatorship administratively.

“Sheila’s deep well of experience will provide strong leadership as Fannie Mae works with the Federal Housing Finance Agency to exit conservatorship while simultaneously fulfilling our mission to provide access to safe, affordable mortgage financing,” Plutzik said in a statement Wednesday announcing Bair’s new position.

Luke Skywalker

unread,

Nov 17, 2020, 6:34:01 PM (yesterday)

to bryndon….@gmail.com, Fannie and Freddie Preferreds and Commons Message Board

4) FHFA replaced division of conservatorship with division of resolutions. This includes the telling retirement of David Fishman.

5) The PSPA was amended to allow capital to build, and timing was sets up for January consent decree.

I admit the Brickman resignation is a head scratcher but there a tons of potential reasons like him being old guard, or crazier theories like Mnuchin wants the job.

Secondly I’ll admit the government’s change in legal posture around “may vs shall conserve“ probably supports your view too.

- 11/16/2020 – capital framework is still not finalized.

latest FHFA report

On May 20, 2020, FHFA announced that it was seeking comments on a notice of proposed rulemaking that establishes a new regulatory capital framework for the Enterprises. A re-proposal of the notice of proposed rulemaking published in July 2018, the proposed rule was published in the Federal Register on June 30, 2020. The comment period for the proposed rule ended on August 31, 2020. To ensure that all comments receive a thorough review and are carefully considered, FHFA will finalize the regulatory capital framework for the Enterprises in early FY 2021.

Fannie Mae Earnings call… https://www.fanniemae.com/newsroom/fannie-mae-news/third-quarter-2020-earnings-media-call-remarks (ed. my bold)

Capital

Turning to net worth and capital, comprehensive income of $4.2 billion increased our net worth to $20.7 billion at the end of the third quarter.

Also in the quarter, our conservatorship capital requirement increased $3.3 billion to $90.8 billion from the second quarter, driven mainly by historically strong acquisition volumes, a reduction in credit risk transfer (CRT) benefit, and the impact of loans in forbearance, which offset a reduction in capital from the impact of continued home price appreciation and an improved acquisition profile.

We anticipate the finalization of FHFA’s proposed capital rule late this year or early next. We estimate that our total regulatory capital requirements under the proposed rule as written would be approximately $160 billion, which includes over $120 billion of Common Equity Tier 1 capital. The increase in capital requirements as compared to conservatorship capital reflects our new buffer requirements, the risk weight floor, and reduced capital relief from CRT.

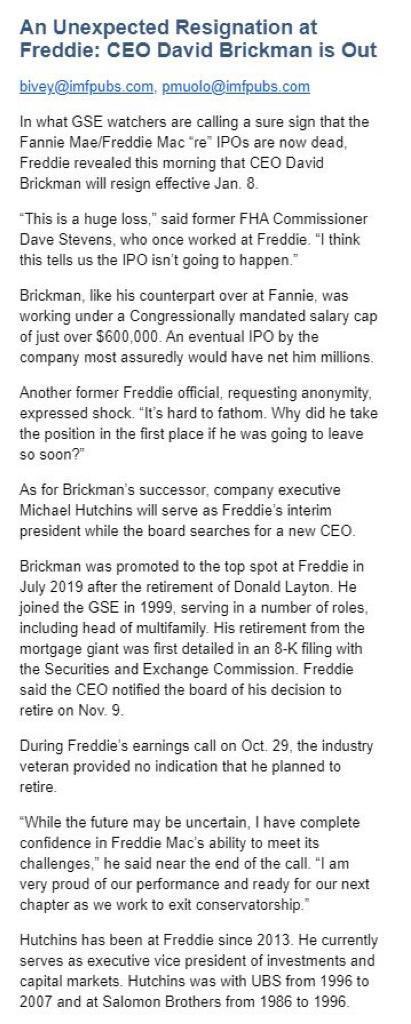

- 11/13/2020 – bad sign for FNMA/FMCC’s release.

Freddie Mac CEO Quits as Prospects Dim for Exit From Government Control

The mortgage giant was taken over during the 2008 financial crisis along with Fannie Mae

WASHINGTON—The chief executive of mortgage-finance company Freddie Mac plans to step down in January, the company said in a securities filing Friday, a surprise move that comes as prospects dim for an exit from government control for the firm and its larger sister, Fannie Mae.

The company gave no explanation for the unexpected departure of David Brickman, 54, a Freddie veteran who had led the company since July 2019.

“This is a personal decision,” a Freddie spokesman said. “After more than 20 years with the company, Mr. Brickman decided that now is the right time to move on and pursue his next chapter.”

- 11/10/2020 – Not sure Bove is right on MC or not, nevertheless, he thinks privatization will happen no matter what

Fannie Mae Privatization: One Analyst Thinks This Needs To Happen

In recent weeks, former Freddie Mac CEO Don Layton wrote two monographs about Fannie Mae and Freddie Mac privatization and GSE reform. Analyst Dick Bove of Odeon Capital read those monographs and set out what he thinks must happen to provide the best possible results for investors.

According to Bove, one of the first things that must be done is to have the senior preferred shares be declared fully paid in both principle and interest. If this doesn’t happen, he says there is no next step. Additionally, the junior preferred shares should pay an initial dividend and then called and replaced with a new issue of preferreds.

Bove also thinks the government should exercise its warrants and argues that Federal Housing Finance Agency Director Mark Calabria must be removed from his position. Bove believes Calabria wants to eliminate Fannie Mae and Freddie Mac and argues that he has taken some steps to do this. However, Tim Pagliara of CapWealth Advisors doesn’t believe Calabria wants to eliminate the government-sponsored enterprises. He has told ValueWalk this in past interviews.

If you believe Bove instead of Pagliara, then supposedly, Calabria won’t allow the GSEs to raise the money needed to function in the private sector. Bove also believes the capital rule as proposed should not be allowed to stand. He argues that it is one of the ways Calabria is using to “cripple” Fannie and Freddie. Pagliara expects the rule to be changed before it is finalized.

Questions raised about Fannie Mae’s Q3 earnings

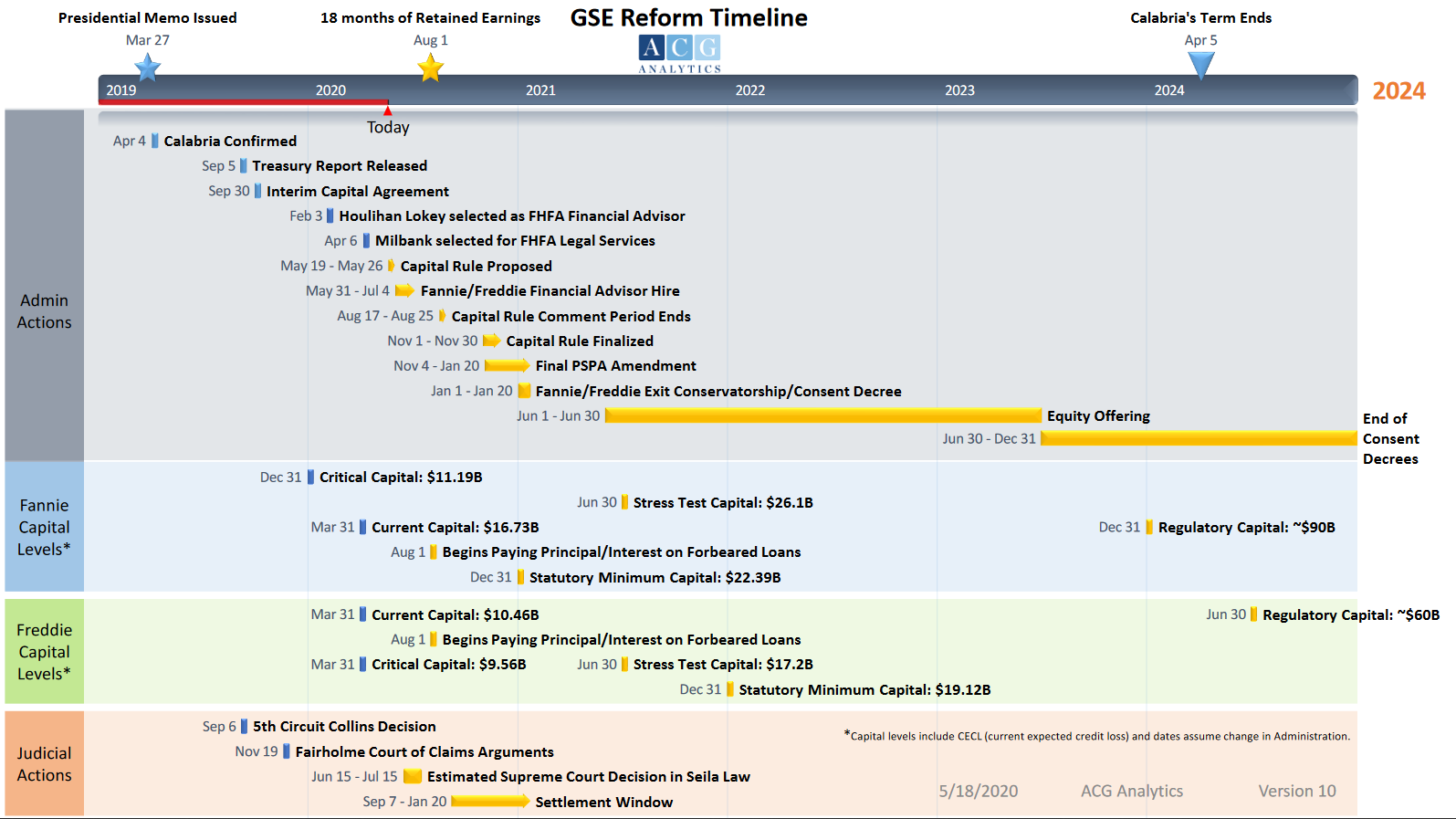

AGC’s new timeline is here:

Clock is ticking on Fannie Mae, Freddie Mac before election

June 19, 2020 Update: If Joe Biden unseats President Donald Trump in the White House, Fannie Mae and Freddie Mac’s progress in exiting conservatorship could be undone. Fox Business reports that housing analysts with ties to Biden’s economic advisers said a Biden presidency could definitely detail the recapitalization and release of the government-sponsored enterprises.

The sources also note that Fannie and Freddie’s fate isn’t a major issue for Biden and his campaign. Instead, he’s more focused on choosing a running mate and strategizing a response to the COVID-19 pandemic, policing and racial equality.

However, they also said that affordable housing is important to the Democratic presidential candidate. Biden reportedly wants to expand the GSEs’ mandate and probably keep them under the control of the government. Thus, his financial advisers suggest that if Biden wins the election in November, he will undo most of the work done by Trump’s housing team, which is headed by Federal Housing Finance Agency Director Mark Calabria and Treasury Secretary Steven Mnuchin.

For one thing, they said if Biden enters the White House, he will try to terminate Calabria and scrap the public offering that would allow Fannie and Freddie to operate as private companies. They said the GSEs would remain in conservatorship and be used to grow homeownership among the low-income population.

It would mean that more Americans would be able to get mortgages, but the net worth sweep could continue, which would be a negative for preferred share holders. One factor they didn’t talk about was the lawsuits that were filed over the preferred shares. If the courts have anything to say about the net worth sweep, the government could be forced to repay what it took from shareholders when the sweep was instituted.

- 11/09/2020 – Officials at the FHFA and Treasury Department have been working on such a release amendment for months

Fannie-Freddie Plan Could Face Race to Finish After Biden’s Win

(Bloomberg) — A White House-backed effort to free mortgage giants Fannie Mae and Freddie Mac from government control has been cast into doubt by former Vice President Joe Biden’s victory over President Donald Trump.

That leaves Trump officials with roughly two-and-a-half months to lock in whatever changes they can to Fannie, Freddie and the nation’s $10 trillion housing-finance system. If they run out of time, it would be a big setback for Fannie and Freddie shareholders, a group that has included hedge fund giants and major Trump donors such as John Paulson of Paulson & Co.

To avoid that outcome, shareholders’ fervent hope is that Mnuchin and Calabria before Jan. 20 come to terms on an amendment to Fannie’s and Freddie’s bailout agreements that Biden can’t unwind. Such an amendment could reduce the government’s massive stake in the companies, making it easier for shareholders to see a higher value on their own stock.

Officials at the FHFA and Treasury Department have been working on such an amendment for months, said a person familiar with the matter, and long have been in agreement on some of the issues that such an amendment would contain. Treasury in 2019 released a housing-finance reform plan that included a list of items that the amendment would address, including limiting Fannie and Freddie’s multifamily businesses and reducing the amount of mortgages the companies can keep in their investment portfolios.

An FHFA spokesman and a Paulson & Co. representative declined to comment. Treasury officials didn’t respond to a request for comment.

Cowen & Co. analyst Jaret Seiberg, in a research note on Friday, wrote that Biden’s Treasury secretary could throw up a roadblock to recapitalizing Fannie and Freddie. But if the Senate remains under Republican control, he wrote, Congress would be less likely to pass legislation to block the FHFA from ending the conservatorships.

- 09/04/2020 – the folly on FNMA/FMCC is going on and on

Opinion Fannie, Freddie lessons learned: The folly of the GSE profit sweep

As the FHFA moves administratively towards an end to the GSEs’ conservatorship, we need a vigorous public debate on these key issues. The folly of the GSE profit sweep shows what can happen when we fail to do that.

- 08/31/2020 – Fannie Mae and Freddie Mac said the re-proposed capital framework will significantly increase the guarantee fees they charge lenders.

GSEs Not Pleased With FHFA’s Re-Proposed Capital Rule

dhollier@imfpubs.com

Fannie Mae and Freddie Mac, in new comment letters filed with the Federal Housing Finance Agency, said the re-proposed capital framework will significantly increase the guarantee fees they charge lenders. Filing their comments on Friday, just before the deadline, the enterprises also suggested the rule could cloud the prospects for any public offerings of stock.

In its comment letter, Fannie estimated the guarantee fee on single-family loans would have to increase by 20 basis points in order for investors to achieve a 10% return on capital. This is a modest return, more in keeping for an investment in a low-risk utility than in a financial institution.

Freddie’s estimate was less precise, but potentially gloomier. “The proposal may require Freddie Mac to increase guarantee fees by 15-35 bps, which may increase housing costs for U.S. consumers,” the GSE said.

Both mortgage giants also criticized the new rule’s treatment of credit risk transfers, which dramatically reduce the amount of capital relief the companies would receive for these transactions. Fannie pointed out that, by de-incentivizing the use of CRT, the proposed rule would increase the GSEs’ reliance on private mortgage insurers, which already represent their largest counter-party risk.

“The capital framework should recognize the risk-reducing nature of CRT and the historical policy support provided by FHFA and Treasury to develop the CRT program,” Freddie said.

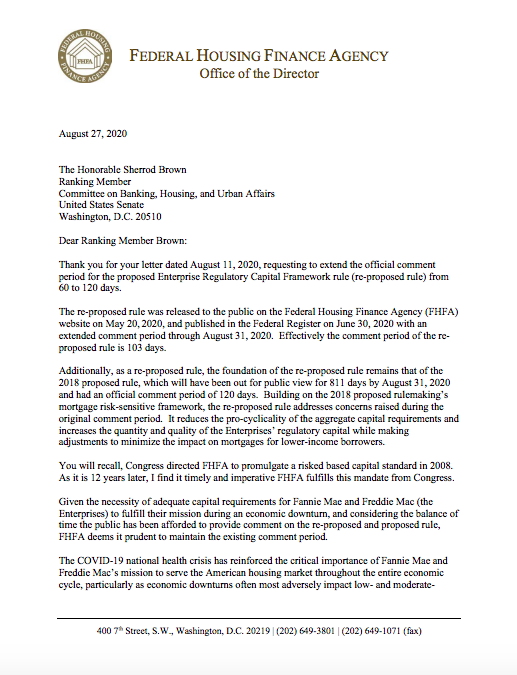

- 08/27/2020 – No extension on comment period: FHFA seems to be determined on the path of release/recap of FNMA/FMCC. Ready to get in the game again?

Hannah Lang@hannahdlang FHFA is not extending the comment period for its proposed capital framework for Fannie Mae and Freddie Mac, with Director Mark Calabria telling@SenSherrodBrown that “FHFA deems it prudent to maintain the existing comment period.”

- 08/19/2020 – The most likely scenario envisions three years of retained earnings with IPO at the end of 2022.

|

- 08/12/2020 – Another great article from Glen B.

Restructuring Frannie Equity Big Bang As Close As 90 Days

- The government took over Fannie Mae and Freddie Mac in 2008 and gave themselves preferred stock and warrants.

- The government then used accounting chicanery to maximize the draw on the Senior Preferred stock, but the true profitability of Fannie and Freddie has forced reversals.

- The government arranged the net worth sweep to kill Fannie Mae and Freddie Mac in 2012.

- Mark Calabria was brought into FHFA because he wrote about how the net worth sweep in 2012 was illegal.

- Fannie and Freddie have begun retaining capital and have retained financial advisors to underwrite an equity offering contingent on an incoming finalized capital rule and equity restructuring.

Gaby has put together a to do list for the recapitalization:

The capital rule comment period ends at the end of this month at which point it can be finalized. The prevailing rumor is that it will be finalized around the end of October. For those of you not familiar with acronyms, the PSPA amendment is the incoming preferred stock purchase agreement amendment as contemplated in the Treasury Housing Reform Plan:

- 08/12/2020 – Dem is dragging the feet of FNMA/FMCC reform. The political hurdle is quite large. Maybe the only way reform can happen is (1) Trump wins election, and/or (2) supreme will signal well to investors and Treasury is willing to settle

Senate Dems join chorus of doubt on proposed GSE capital rule

Senate Democrats are pushing the director of the Federal Housing Finance Agency to extend the comment period for a proposed new capital framework for Fannie Mae and Freddie Mac.

On Tuesday, Sen. Sherrod Brown (D-Ohio), ranking member of the Senate Banking Committee, and nine other Senate Democrats sent a letter to FHFA Director Mark Calabria urging him to “allow for more thoughtful feedback” on the new rule, which they said was too complex for the original 60-day comment period to allow for meaningful input from all stakeholders.

In a report to Congress in June, Calabria said that Fannie and Freddie were “inarguably undercapitalized for their size, risk, and systemic importance,” and that the GSEs would not be able to withstand a serious economic downturn. Calabria said the new capital requirement – outlined in a 424-page rule released for public comment May 20 – would require Fannie and Freddie to become “safe and sound” financial institutions in order to exit conservatorship. This means they would be required to have enough capital to enable them to weather economic downturns.

However, Brown and his fellow senators said the rule needed to be more carefully scrutinized before implementation.

“The capital framework that FHFA ultimately adopts will affect not just the Enterprises but the entire housing finance system and the millions of homeowners and renters who depend on it,” they wrote. “It will help determine what types of loan products are available, to whom, through which channels, and at what price. It will also determine what types of resources the Enterprises have to continue serving all parts of the housing market at all times. We must all understand the effects of the rule on renters and homeowners, especially those who have historically been underserved by our housing finance system, before a final rule is adopted.”

The senators said that they did not believe that 60 days was enough time “for all stakeholders to thoroughly review” the proposal – especially during a pandemic.

“The coronavirus pandemic has required the entire country to turn its attention to adapting to new work environments, prioritizing health, and responding to the economic needs of the millions of families who are struggling to stay in their homes,” they wrote. “Stakeholders wishing to provide comment on this critical rule will not have the time and attention that they otherwise might give to analyzing and providing insights on the rule.”

The lawmakers also demanded that the FHFA provide an analysis of the effects the new rule would have “on various populations of homeowners and renters.”

“This includes the effects on small lenders and the affordable rental housing community,” they wrote.

Brown and his colleagues aren’t the first to voice concerns over the proposed rule. Last month, Rep. Maxine Waters (D-Calif.), Rep. William Lacy Clay (D-Mo.) and Rep. Denny Heck (D-Wash.) said in a letter to Calabria that the FHFA should prioritize economic recovery and delay the rule until after the pandemic had passed.

Waters, Clay and Heck also said they were “very concerned” that the new capital rule would slow the nation’s economic recovery from the COVID-19 crisis by increasing borrowing costs and hampering the GSEs’ ability to provide liquidity for the housing market. They further said that they were concerned that the new rule would negatively impact minority borrowers.

- 08/11/2020 – FNMA/FMCC are the most profitable companies per employee. Hopefully it can survive politically

These 18 big companies made more than $250,000 in profit per employee last year

- 08/07/2020 – Good to know Paulson is still strongly supporting Trump

Billionaire former hedge fund chief John Paulson to host big-money Hamptons fundraiser for Trump

- President Trump is set to attend a big-money fundraiser Saturday at the home of one of his closest Wall Street allies.

- Billionaire former hedge fund manager John Paulson will host Trump at his home in swanky Southampton, according to people with direct knowledge of the matter.

- Tickets for the dinner event are priced up to $500,000 per couple, an invitation says.

- 07/28/2020 – relative long and uncertain road for preferred to reach par.

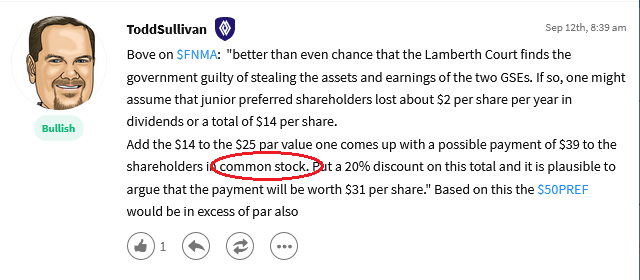

WHAT SHOULD FANNIE MAE JUNIOR PREFERRED SHARES BE WORTH?

Fannie Mae and Freddie Mac junior preferred shares could increase by at least 100% if one analyst is correct. Dick Bove of Odeon Capital said Josh Rosner of Graham Fisher & Co., who has testified multiple times in front of Congress about the government-sponsored enterprises, discussed them with the Odeon team.

Among the talking points was the likelihood that negotiations on what to do about the GSEs will have to begin, leading to a resolution by the time of the inauguration date of the winner of the presidential election. Bove believes the end result for holders of Fannie Mae junior preferred shares is at least a 100% increase in the value of the stock.

Fannie Mae junior preferred shares and the Collins case

Rosner said it is in the government’s best interest to settle with the plaintiffs before the Supreme Court in the Collins case. If the government loses, it could own Fannie Mae and Freddie Mac $130 billion. Additionally, the Federal Housing Finance Agency could be declared unconstitutional, and the next president could fire FHFA Director Mark Calabria. However, these last two points have already effectively happened due to the impact of the Seila case on the government-sponsored enterprises.

If the government wins the Collins case, it will still have to eliminate the senior preferred shares and the net worth sweep if it wants to recapitalize and release Fannie and Freddie from their conservatorships. The government has already spent more than $100 million on legal fees and achieved nothing but “maintenance of the status quo,” Bove added.

Also if the government wins, it will create a precedent in which the federal government can take whatever it chooses from possibly any company whenever it chooses to do so, striking at the heart of private property rights.

Bove believes the president, the Treasury secretary and FHFA director are united in their belief that Fannie and Freddie must be recapitalized and released from conservatorship. To do this, the lawsuits over the Fannie Mae and Freddie Mac junior preferred shares will have to be settled. The senior preferred shares and the net worth sweep will also have to be eliminated.

Here are the negotiables

In the negotiations over the Fannie Mae and Freddie Mac junior preferred shares and the Collins case, the government will want clear indications that both GSEs are truly safe and sound. Bove believes the government will also want some control over the companies.

He also expects the government to want a commitment fee of possibly 10 to 15 basis points for any government guarantees on 30-year fixed-rate mortgages. Additionally, the government will want freedom from a political problem “no one wants to deal with.” He believes Joe Biden, if elected, would probably be happy if he never had to deal with Fannie and Freddie.

In exchange, investors will want the standing and rights of Fannie Mae and Freddie Mac junior preferred shares to be restored along with their lost dividends. They will also want to see value created for common shareholders.

Issues with the Fannie Mae junior preferred shares that must be resolved

In order for both sides to agree on the matter, several issues must be addressed. For example, Bove said the FHFA’s failures to meet certain requirements of the Housing and Economic Recovery Act of 2008 will have to be corrected. He also said some internal government issues must be corrected, and a capital rule must be put in place.

Fannie Mae and Freddie Mac will have to hold public offerings, and the GSEs may have to acquire government warrants.

Bove doesn’t expect to see dividend payments on the Fannie Mae and Freddie Mac junior preferred shares. He also doesn’t expect the junior preferred shares to be converted into common shares or full payment of par value on preferreds.

He also gave an expected timeline for the recapitalization and release process. By late September, all comments on the proposed capital rule will have been received, and the rule will be in place by late October. By mid-November, he expects a resolution of the senior preferred shares, possibly eliminating the Supreme Court decision.

Also in November, he expects the GSEs to submit their required capital data. Then in December, he expects the resolution to begin ahead of a target date for the resolution in mid-January.

- 07/23/2020 – CHLA’s comment on recap capital rule

https://documentcloud.adobe.com/link/review?uri=urn:aaid:scds:US:dfd3a82a-930a-46d7-99f6-d8da39c15561#pageNum=1

- 07/22/2020 – one bash from Bloomberg on commons

Fannie Mae Draws a Zero-Dollar Price Target Due to Dilution

Federal National Mortgage Association drew an underperform rating and a price target of zero dollars from Wedbush analyst Henry Coffey, who started coverage Tuesday. In May the Federal Housing Finance Agency proposed that Fannie Mae and fellow mortgage giant Freddie Mac be required to hold hundreds of billions of dollars in capital to guard against losses.

Despite the “tremendous underlying value” in the company, any recapitalization of Fannie Mae is likely to result in substantial dilution to public shareholders, Coffey wrote in a report. He is one of two sell ratings among six analysts tracked by Bloomberg. The shares closed Tuesday at $2.09.

“Our estimates suggest that in the process of recapitalizing Fannie Mae, there will be little or no value left over for current public shareholders, and that any residual value accruing to them will be greatly diluted by Treasury’s warrant,” Coffey said. That warrant covers roughly 80% of the shares outstanding when exercised and expires in September 2028.

- 07/22/2020 – IMF news

- 07/22/2020 – convincing argument from Boyle capital

Great summary by Boyle Capital that details current issues and trajectory of GSE recap and release. Outstanding work. boylecapital.com/news-and-insig

full article (Equity July 2020 No CRS)

The en banc plaintiffs appealed this decision to the Supreme Court where it was distributed for conference (Collins v Mnuchin 19-422) on January 10, 2020, and held until after Seila was released on June 29th. It was taken in conference again on July 1st and July 8th with the order granting certiorari being issued on July 9th. While oral arguments have yet to be scheduled, the Supreme Court term starts in October and generally lasts nine months. Given the already crowded Supreme Court schedule for October and November, it is unlikely the hearing will be scheduled prior to the first of next year.

To think that Treasury would spend the better part of two years working on a plan to end the conservatorships of Fannie and Freddie and the FHFA would put out a capital rule, hire financial and legal advisors, only to take a knee on the 1-yard line seems unlikely. The puzzle has been laid out for those paying close attention and it is our strong conviction that the final pieces will be put in place by Secretary Mnuchin and Director Calabria regardless of the election outcome this fall. When those final pieces are put in place, we expect the preferred shares to appreciate substantially.

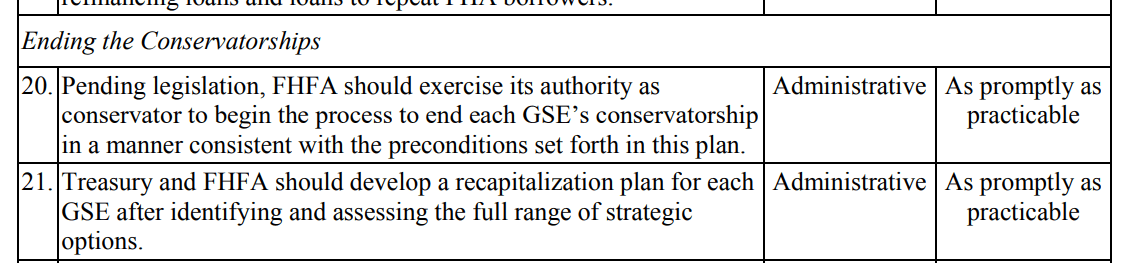

What would happen in the event Joe Biden wins the election and the Democrats end up with control of Congress? The bipartisan Housing Economic Recovery Act (HERA) requires the FHFA to fix Fannie and Freddie and release them from conservatorship and gives the FHFA broad authority in order to carry out that mission. In the interim agreement entered last September between FHFA (as conservator) and Treasury, allowing Fannie and Freddie to retain additional capital, Treasury and the FHFA agreed to negotiate and execute an additional amendment to the PSPA consistent with the recommendations set forth in Treasury’s September 2019 Housing Reform Plan. Once the Net Worth Sweep is ended and the senior liquidation preference is written down in the previously contemplated PSPA amendment, there is little a Biden administration could do.

In a February response letter to Senator Mark Warner seeking further details from Secretary Mnuchin and Director Calabria on their plans, Director Calabria referenced the use of a consent decree as a potential means to accelerate the release of the GSEs from conservatorship. According to Calabria, “under a consent decree, FHFA would have the authority to permit an Enterprise that has reached a certain capital level below the required minimum to operate outside of conservatorship subject to a capital restoration plan….Methods for modifying a consent order are either provided for in the consent order itself or agreed to by both parties.”

A consent decree can only be modified by the parties to the agreement, which in this case would be the FHFA, Fannie Mae and Freddie Mac. In the event of a Biden victory this November, Calabria and Mnuchin would be well within their authorities under HERA to execute an amendment to the PSPA (ending the Net Worth Sweep and eliminating the senior liquidation preference) and a consent decree with Fannie and Freddie prior to inauguration day. If they were to combine these actions with a legal settlement with shareholders, there would be nothing a new administration could do to alter the path forward without changing HERA and that would require 60 votes in the Senate which is unlikely (Republicans currently control 53 seats and Democrats 45 seats).

Settling with the Collins plaintiffs would also render the case before the Supreme Court moot and mean that Director Calabria would be insulated from immediate removal by the Biden administration. The Seila decision would provide the Biden administration a path for removing Calabria, but it would likely take several years to play out through the courts; thereby giving Calabria additional time for administrative action should he want it.

- 07/15/2020 – good chance for investors to win?

Supreme Court Decisions Clear the Way for Ending the Net Worth Sweep

The U.S. Supreme Court wrapped for the year with a pair of decisions that could bode well for ending the government’s Net Worth Sweep of Fannie Mae and Freddie Mac’s earnings and help secure an equitable solution for shareholders in the government sponsored enterprises.

With an assist by the Supreme Court, the Administration can take steps to end the largest unconstitutional and unauthorized taking in U.S. financial history and make it more likely investors and shareholders will infuse Fannie and Freddie with more capital, confident that the government can again be trusted to abide by the law. There has never been a better time to address the last piece of unfinished business from the 2008-09 financial crisis.

Supreme Court to Review Who Gets to Keep $300 Billion in Fannie Mae-Freddie Mac Profits

In its statement granting the case one-hour of oral argument during the term beginning in October, the Supreme Court will decide two questions. First, does the structure of the Federal Housing Finance Agency (FHFA) violate the constitutional separation of powers. Second, “must the courts set aside a final agency action” taken when the FHFA was illegally structured and, as a result, “strike down the statutory provisions that make FHFA independent.”

The issues echo elements of the recent Supreme Court decision that the U.S. president could replace the director of the Consumer Financial Protection Bureau (CFPB) without cause but validating the agency’s existence and actions.

- 07/13/2020 – privatizations are still on track

Why Fannie Mae and Freddie Mac Privatizations Are Still On Track

- 07/11/2020 – “The justices will hear the case in the nine-month term that starts in October.” so we still need to wait and see.

Fannie-Freddie Profit Sweep Draws U.S. Supreme Court Review

By Greg Stohr

July 9, 2020, 11:12 AM PDT Updated on July 9, 2020, 2:08 PM PDT

The U.S. Supreme Court agreed to decide whether investors can challenge the 2012 agreements that let the federal government collect hundreds of billions of dollars of Fannie Mae and Freddie Mac’s profits.

The justices said they will hear an appeal by President Donald Trump’s administration of a ruling that would force the government to defend against a shareholder lawsuit. The investors say the agreements exceed the authority of the Federal Housing Finance Agency, which regulates the two mortgage giants.

A ruling in the investors’ favor would give them a chance to collect a massive settlement. Fannie and Freddie have paid more than $300 billion in dividends to the Treasury under the so-called net-worth sweep.

The administration told the court the dispute “is of immense practical importance.” The justices will hear the case in the nine-month term that starts in October.

The Supreme Court on Thursday also agreed to hear an appeal from shareholders challenging the profit sweep under a different legal theory.

Fannie Mae and Freddie Mac keep the U.S. housing market humming by buying mortgages from lenders and packaging them into bonds that are sold to investors with guarantees of interest and principal.

‘Cloud of Uncertainty’

After the housing market cratered in 2008, the companies were put into federal conservatorship and sustained by taxpayer aid. They have since returned to profitability and paid $115 billion more in dividends to the Treasury than they received in bailout funds. Since 2013, most of their profits have been sent to the Treasury under the net-worth sweep.

The administration contends the 2008 law that set up the FHFA precludes lawsuits that challenge the profit sweep. The law bars courts from doing anything to “restrain or affect the exercise of powers or functions of the agency as a conservator.”

A splintered New Orleans-based federal appeals court let the lawsuit go forward, saying the FHFA wasn’t acting as a conservator when it agreed to the net-worth sweep.

The suing shareholders said the appeals court reached the right conclusion. But they nonetheless urged the Supreme Court to hear the Trump administration appeal, saying all sides would benefit from clarity.

“So long as there is a credible threat that litigation will invalidate the net-worth sweep, a cloud of uncertainty will hang over the companies’ capital structure,” the shareholders told the Supreme Court. “Investors will not be willing to supply the tens of billions of dollars in new capital that are essential to Treasury’s reform plan.”

“FHFA looks forward to the U.S. Supreme Court taking up” the case and clarifying the issues involved, the agency said in a statement.

Trump administration officials, including Treasury Secretary Steven Mnuchin, have long stated that they want to end federal control by releasing Fannie and Freddie from conservatorship. Wall Street analysts have said they are skeptical of that happening before the November election, meaning the administration’s goal largely depends on Trump winning a second term.

The government’s appeal is Mnuchin v. Collins, 19-563, and the shareholders’ appeal is Collins v. Mnuchin, 19-422.

- 07/10/2020 – the scuttlebutt for a quick settlement coming?

Short Takes: SCOTUS and the Conservatorship / FHFA Extends Origination Flexibilities / Freddie Expands Board

dhollier@imfpubs.com

Speaking of IPOs, the litigious shareholders of Fannie Mae and Freddie Mac seem pretty sure that SCOTUS’ Seila decision – and especially the addition of Collins v. Mnuchin to its upcoming calendar – bodes well for a quick end to the conservatorship and successful re-IPOs for Fannie and Freddie. The scuttlebutt in legal circles is SCOTUS has put pressure on Treasury to negotiate with shareholders. At least that’s what one attorney involved in the litigation told Inside Mortgage Finance. Of course, shareholders have been saying that for years…

In a sign that there’s still no sign of the coronavirus crisis coming to an end, the Federal Housing Finance Agency announced yesterday that Fannie and Freddie will be extending their relief policies for home buyers. All these increased flexibilities, including alternative appraisal and employment verification methods, were supposed to expire July 31, but FHFA has extended the deadlines until at least the end of August…

Freddie has added Beazer Homes CEO Allan Merrill and Paul Schumacher, founder of Schumacher Homes, to its board.

- 7/09/2020 – Good to know that Supreme Court is going to hear the GSE case and make final decision by June 2021. It seems like a settlement is close, maybe right after election day.

Supreme Court to Hear Case on Government Seizure of Fannie, Freddie Profits

Case, to be heard during court’s next term, involves the federal takeover of the mortgage-finance companies

The Supreme Court likely will hear the cases near the end of the year, with decisions expected by June 2021.

- 06/26/2020 – when we will have the relisting?

InMortgageFinance @IMFpubs

The next step for the government-sponsored enterprises, now that they’ve chosen underwriting financial advisors, will probably be relisting their stock on a nationally recognized exchange.

- 06/15/2020 – FNMA and FMCC have found their financial advisers, so the R&R is coming?

Fannie Mae and Freddie Mac announce underwriting advisers

J.P. Morgan and Morgan Stanley will guide the GSEs as they end conservatorship

Announcing the advisers in the middle of the worst health crisis to hit the U.S. in more than a century underscores the Trump administration’s determination to end government control of the mortgage giants before “election risk” gets in the way. That’s the polite term pundits use to highlight the possibility that President Donald Trump may lose the election in November, which would leave Democrats to decide the fates of the two companies.

The newly announced advisers will help take Fannie and Freddie through steps that are necessary to leave federal conservatorship, including reviewing their business plans and strategies for recapitalizing the companies.

“We look forward to working with J.P. Morgan to continue meeting the milestones necessary to begin our new chapter as soon as possible,” said David Brickman, Freddie Mac’s CEO. “At the same time, our focus on supporting borrowers, renters and lenders in the face of COVID-19 is stronger than ever.”

| seysmont |

Jun 14

|

I’m waiting for SPS amendment. There is really nothing going on. SPS action solidifies the path of recap that Biden won’t be able to undo. It’s coming soon.

On the way in, in the summer of 2008, the GSE’s registered all JPS with the SEC. They weren’t registered with the SEC before the c-ship action. That deregistering of the convert that converted is a cue for getting current with all the SEC filing. Some corp action is coming within the next 2 months. If the advisers are coming in the next few weeks, maybe the uplisting is coming, and SPS rework should be coming as currently the equity is all claimed by the SPS.

- 06/09/2020 – MK on committee hearing

FULL COMMITTEE HEARING Oversight of Housing Regulators

- 06/08/2020 – another blow (not surprising) to the investors

Case dismissed. Jones Day plaintiffs – Mason, Owl Creek, Appaloosa, Akanthos & CSS. Direct claims do not survive.

- 06/03/2020 – Schmerin believes a closer reading of the rule indicates that they will only have to raise about $135 billion and possibly even less than that.

Fannie Mae’s release from conservatorship progresses

Analyst Dick Bove said Schmerin believes Fannie and Freddie will continue to move toward exiting conservatorship no matter which party controls the White House. He also believes the U.S. needs the GSEs to support its home finance markets and that releasing them from conservatorship will better enable them to do what they need to do.

He cited four steps that have been taken to show the process that has moved Fannie Mae and Freddie Mac toward the end of their conservatorships. The FHFA hired advisors to release them, and each of the GSEs is seeking its own advisors as well. The FHFA is also building its staff, recently with the addition of Kate Fulton as chief operating officer. Further, the agency released the new capital rule for Fannie and Freddie.

Ongoing issues

Regarding the new capital rule, Schmerin believes press reports and commentary are misleading because they suggest the new capital rule requires Fannie Mae and Freddie Mac to raise more than $240 billion and achieve a 3.85% equity to asset ratio.

Instead, he believes that a closer reading of the rule indicates that they will only have to raise about $135 billion and possibly even less than that. Bove did not offer any explanation as to why all the other commentary on this issue might be wrong.

- 05/30/2020 – Howlett value FNMA at $5 in short term, and $9 in 2024. Maybe attractive after election.

Fannie Mae Might Become a Dividend Payer Again

Howlett now expects Fannie Mae to raise $55 billion of capital in the summer of 2021. He sees $15 billion coming from newly issued shares, another $30 billion in mandatory convertible preferred stock, and another $10 billion in non-cumulative preferred stock. Howlett further sees the 2021 capital raise potentially being followed by three additional preferred stock offerings of $10 billion each in 2022 and 2023 and a larger $20 billion in 2024. His report said:

Our model forecasts that Fannie will enter the capital raise with $20 billion of statutory capital post the full write-down on the Treasury’s senior preferred stock and then generate $54 billion of internal capital over the following 12 quarters. Fannie Mae will likely reach $174 billion of capital by the third-quarter of 2024 (includes 10% buffer) and then become a dividend paying company.

Howlett’s price target of $5 on Fannie Mae has not been revised, but this still implies that the shares could double in time. And longer-term, with a dividend in hand, Howlett sees the case for Fannie Mae shares to even reach $9 out in 2024.

- 05/27/2020 – According to Tim Howard and, this new recap plan is as bad as it is. Too high level of required capital. Very hard to attract investors to come in. I might need to sell this small position for other good ones.

Well, now we know. The Fannie Mae and Freddie Mac capital standards put out for comment last Wednesday by the Federal Housing Finance Agency (FHFA) under Director Mark Calabria openly and unapologetically call for the companies to operate under a capital regime and capital requirements designed for commercial banks—in spite of the fact that the companies are not banks, have no business in common with banks, and have historical mortgage delinquency and credit loss rates one-third those of banks. By imposing these standards, FHFA has made it a condition of Fannie and Freddie’s future emergence from conservatorship that they function at a fraction of their potential efficiency, with severe negative impacts on homebuyers, particularly those with low and moderate incomes.

THE NEW PROPOSED CAPITAL RULE FOR FREDDIE MAC & FANNIE MAE: TEN QUICK REACTIONS (Don Layton)

- 05/21/2020 – new proposal of recap plan is completed. pfs and commons spike and retreat somewhat, same old story. The following catalysts might can from court decision or news. should watch out closely.

Fannie Mae & Freddie Mac Litigation, FNMA, FMCC updated May 19, 2020

19-422 Patrick J Collins v. Mnuchin (Pending petition SCOTUS) .…Common & Preferred, Derivative

Claim: “for cause” separation of powers §?4512(b)(2)

https://www.scotusblog.com/case-files/cases/collins-v-mnuchin/

(Decided according to David Thompson 1 week after resolution in Seila Law, ~first week of july-2020)

19-563 Mnuchin v. Patrick J Collins (Pending petition SCOTUS)…….Relates to all cases

Claim: § 4617(f) prevents ruling on 3th amendment, § 4617(b)(2)(A) (i) forbids challenging the Third Amendment

(Decided according to David Thompson 1 week after resolution in Seila Law, ~first week of july-2020)

https://www.scotusblog.com/case-files/cases/mnuchin-v-collins/

13-1053 (14-5254) (1:13-cv-01053)

Fairholme Fund, Inc. v. FHFA……Preferred, Direct & Derivative

Honorable: Royce C. Lamberth

Claim: 3th amendment, breach of fiduciary duty, breach of contract, breach of the implied covenant of good faith and fair dealing

District Court for the District of Columbia

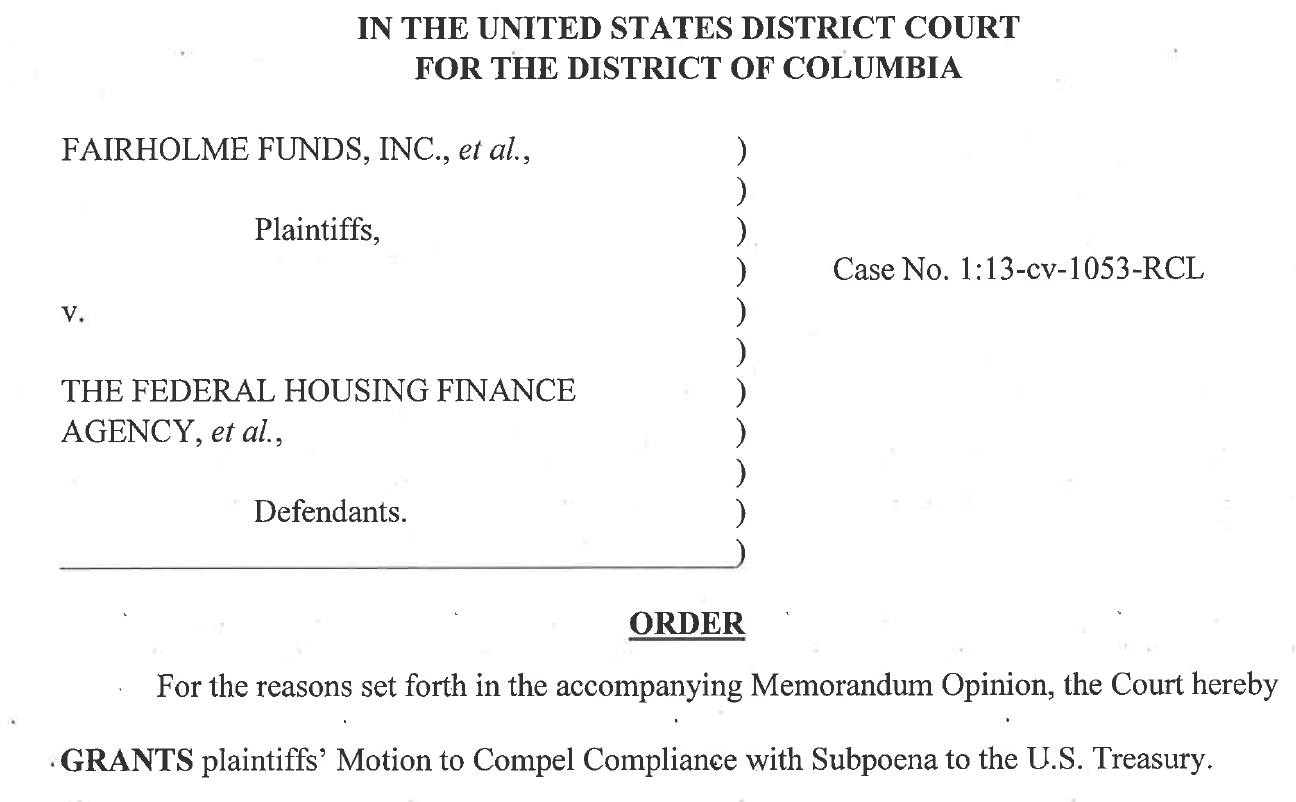

RFP’s Granted

https://www.courtlistener.com/docket/4212077/fairholme-funds-inc-v-federal-housing-finance-agency/

Fact discovery was to close on April 30, 2020, Trial was set for March 31, 2021 (with a pretrial 30-60 days before)

May 9, 2020 – The deadlines in the Second Amended Scheduling Order are hereby adjourned

pending further order of this Court, The parties are directed to submit proposed amended deadlines no later than June 30, 2020. https://www.courtlistener.com/recap/gov.uscourts.dcd.160910/gov.uscourts.dcd.160910.118.0.pdf

13-1288 (1:13-mc-01288)

In re Fannie Mae/Freddie Mac Senior Preferred Stock Purchase Agreement

Class Action Litigations ………………………… Common & Preferred, Class Action, Direct & Derivative

Honorable: Royce C. Lamberth

District Court for the District of Columbia

Plaintiffs demand a Trial by Jury

Direct claim, breaches of contract, breaches of the implied

covenant of good faith and fair dealing, breaches of fiduciary duties,

and violations of Delaware and Virginia law governing dividends

If the Direct claims is denied it also claims these Derivative: breaches of fiduciary duty, compensatory damages and disgorgement, breached the terms of the certificates of designation and the implied covenant of good faith and fair dealing, appropriate equitable and injunctive relief to remedy breaches of contract, breaches of the implied covenant of good faith and fair dealing, breaches of fiduciary duty, and violations of Delaware and Virginia Corporate law, including rescission of the Third Amendment. https://www.courtlistener.com/recap/gov.uscourts.dcd.163155/gov.uscourts.dcd.163155.71.0.pdf

https://www.courtlistener.com/docket/4212341/in-re-fannie-maefreddie-mac-senior-preferred-stock-purchase-agreement/

The Class:

1) N. Bradford Isbell ……. Common

2) Michelle M. Miller …… Common

3) Charles Rattley ………… Common

4) Timothy J. Cassell …… Common

5) 111 John Realty Corp… Preferred

8) United Equities Commodities Com ….. Preferred

6) 1:13-cv-01149 Joseph Cacciapalle ….. Preferred

7) 1:13-cv-01421 Marneu Holdings, Co .. Preferred

9) 1:13-cv-01169 American European Insurance Co … Preferred

10) 1:13-cv-01443 Barry P. Borodkin ……. Preferred

11) 1:13-cv-01094 Mary Meiya Liao ……. Preferred

https://www.courtlistener.com/docket/4212341/in-re-fannie-maefreddie-mac-senior-preferred-stock-purchase-agreement/

Fact discovery was to close on April 30, 2020, Trial was set for March 31, 2021 (with a pretrial 30-60 days before)

May 9, 2020 – The deadlines in the Second Amended Scheduling Order are hereby adjourned

pending further order of this Court, The parties are directed to submit proposed amended deadlines no later than June 30, 2020.

https://www.courtlistener.com/recap/gov.uscourts.dcd.160910/gov.uscourts.dcd.160910.118.0.pdf

May 9, 2020 –Document 118 Order on Motion for Miscellaneous Relief

13-1439 (1:13-cv-01439)

Arrowood Indemnity Company v. Fannie Mae……Preferred, Direct & Derivative

Honorable: Royce C. Lamberth

Claim: 3th amendment, breach of fiduciary duty, breach of contract, breach of the implied covenant of good faith and fair dealing

District Court for the District of Columbia

https://www.courtlistener.com/docket/6995674/arrowood-indemnity-company-v-federal-national-mortgage-association/

Fact discovery was to close on April 30, 2020, Trial was set for March 31, 2021 (with a pretrial 30-60 days before)

May 9, 2020 – The deadlines in the Second Amended Scheduling Order are hereby adjourned

pending further order of this Court, The parties are directed to submit proposed amended deadlines no later than June 30, 2020. https://www.courtlistener.com/recap/gov.uscourts.dcd.160910/gov.uscourts.dcd.160910.118.0.pdf

16-3113 (4:16-cv-03113)

Patrick J Collins v. Lew …………………….…Common & Preferred, Derivative

Honorable: Judge Nancy F Atlas in District Court

Claim: “for cause” separation of powers §?4512(b)(2)

https://www.courtlistener.com/docket/4533994/collins-v-lew/

After appeal 17-20364, the 5th circuit remanded this back to Judge Nancy F Atlas in District Court, S.D. Texas, after a decision in Seila Law it will proceed (~first week of july-2020)

17-497 (1:17-cv-00497)

Rop v. Federal Housing Finance agency…….Common & Preferred, Derivative

Honorable: Paul L. Maloney

Claim: voiding 3th amendment & “for cause” separation of powers and

striking down HERA 12 U.S.C. §§ 4511(a), 4512(b)(2), and 4617(a)(7)

District Court, W.D. Michigan

https://www.courtlistener.com/docket/13521280/rop-v-federal-housing-finance-agency/

No next Date available (waiting on Collins, document 64 says “notice of supplemental authority concerning Collins v. Mnuchin” http://www.glenbradford.com/wp-content/uploads/2019/09/17-cv-00497-0064.pdf )

18-2506 (17-2185) (0:17-cv-02185)

Atif F. Bhatti vs. FHFA……………Common & Preferred, Derivative

Honorable: Patrick Joseph Schiltz

District Court, D. Minnesota

Claim: 3th amendment & “for cause” separation of powers §?4512(b)(2)

https://www.courtlistener.com/docket/7379258/bhatti-v-federal-housing-finance-agency-the/

On appeal in the 8th circuit, Oral Argument 10/15/2019

http://media-oa.ca8.uscourts.gov/OAaudio/2019/10/182506.mp3

https://www.courtlistener.com/audio/65849/atif-bhatti-v-federal-housing-finance-agency/

(The court strives to issue the opinion within 90 days after oral

Argument or submission to a nonargument panel. http://media.ca8.uscourts.gov/newrules/coa/iops06-19update.pdf)

18-3478 (2:18-cv-03478)

Wazee Street Opportunities v. United States………Common, Class action, Derivative

Honorable: Nitza I Quinones Alejandro

Claim: voiding 3th amendment & “for cause” separation of powers

District Court, E.D. Pennsylvania

https://www.courtlistener.com/docket/7681282/wazee-street-opportunities-fund-iv-lp-v-the-federal-housing-finance-agency/

waiting on Collins as document 38 says Supplemental authority filed by Defendant ….. in the matter of Collins v. Mnuchin, No. 17-20364, now 19-422 / 19-563)

19-7062 (1:18-cv-01142)

Joshua J. Angel v. BOD of FNMA,FMCC & FHFA-C ….….Preferred, Direct

Previously assigned to: Honorable: Royce C. Lamberth (18-1142)

https://www.courtlistener.com/docket/6880882/angel-v-federal-home-loan-mortgage-corporation/

Claim: Breach of quarterly BOD duties

District Court for the District of Columbia

It was Decided april 24, 2020: We affirm. The district court properly dismissed Angel’s initial complaint as time-barred.“ ORDERED and ADJUDGED that the decision of the district court be AFFIRMED”

This case is lost on the statute of limitation and not on merit

http://www.glenbradford.com/wp-content/uploads/2020/04/19-7062-1839674.pdf

—————————————————————–

Cases in Sweeney’s U.S. Court of Federal Claims

—————————————————————–

20-121 (20-122) (13-465C) (1:13-cv-00465) (17-1122)(17-104)

FAIRHOLME FUNDS, INC. v. United States………..Common & Preferred, Direct & Derivative

Honorable: Margaret M. Sweeney

United States Court of Federal Claims

Claim: **SEALED** 413 AMENDED COMPLAINT (Entered: 03/08/2018)

Redacted version without coercion attacks available at:

https://www.docketbird.com/court-documents/Fairholme-Funds-Inc-et-al-v-USA/REDACTED-DOCUMENT-filed-by-ACADIA-INSURANCE-COMPANY-ADMIRAL-INDEMNITY-COMPANY-ADMIRAL-INSURANCE-COMPANY-ANDREW-T-BARRETT-BERKLEY-INSURANCE-COMPANY-BERKLEY-REGIONAL-INSURANCE-COMPANY-CAROLINA-CASUALTY-INSURANCE-COMPANY-CONTINENTAL-WESTERN-INSURANCE-CO/cofc-1:2013-cv-00465-00422

March 9, 2020 the interlocutory appeal was granted the

CFC identified six “controlling questions of law” raised by its order, the first three of

which pertain to the CFC’s decision to dismiss Petitioners’ direct claims:

(1) Whether the court lacks subject-matter jurisdiction over plaintiffs’ direct

claims for breach of fiduciary duty and breach of implied-in-fact contracts.

(2) Whether plaintiffs who purchased stock in Fannie and Freddie after the

PSPA amendments lack standing to pursue their direct claims.

(3) Whether plaintiffs lack standing to pursue their self-styled direct claims

because those claims are substantively derivative in nature.

The last three controlling questions identified by the CFC related to its decision

to deny the motion to dismiss Petitioners’ derivative claims:

(4) Whether plaintiffs have standing to assert derivative claims notwithstanding HERA’s succession clause.

(5) Whether the [FHFA-as-conservator’s] actions are attributable to the United States such that the court possesses subject-matter jurisdiction to entertain plaintiffs’ derivative takings and illegal exaction claims.

(6) Whether plaintiffs’ allegations that the FHFA entered into an implied-in-fact contract with the Enterprises to operate the conservatorships for shareholder benefit fail as a matter of law.

http://www.glenbradford.com/wp-content/uploads/2020/03/20-121-0002.pdf

By no later than 14 days after the completion of that process (interlocutory appeal), the parties shall file a joint status report in which they propose further proceedings, if any are necessary.

The following List Of Fannie Mae and Freddie Mac Shareholder Suits are Pending In The Court Of Federal Claims awaiting a decision in the Fairholmes interlocutory appeal, with below each group their stand on the interlocutory appeal, and further replies

1) 13-466C Joseph Cacciapalle ………..………… Preferred, Class Action, Direct*

2) 13-496C American European Insurance.…. Preferred, Class Action, Direct

3) 13-542C Francis J. Dennis ………………….…. Preferred

March 27, 2020 above 3 Plaintiff’s think none of their counts should be dismissed

4) 13-385C Washington Federal v. United States . Common & Preferred, Class Action, Direct*

April 2, 2020 Plaintiff argues None of the claims in Fairholme apply to their case

April 16, 2020 the government thinks:

a) Fannie Mae And Freddie Mac Shareholders Lack Standing To Assert Substantively-Derivative Claims As Direct Claims

b) The Court Lacks Jurisdiction To Review The Merits Of The Enterprises’ Placement In Conservatorship

c) The Washington Federal Plaintiffs May Not Pursue Derivative Claims

5) 13-608C Bryndon Fisher (FNMA) ………….. Common Derivative*

6) 14-152C Bruce Reid (FMCC) …………………… Common Derivative*

May 18, 2020 Fisher/Reid file motion to certify interlocutory appeal

7) 13-672C Erick Shipmon……..…………………… Common Derivative

March 27, 2020 above 3 Plaintiff’s think their claim is substantially the same as Fairholme’s

April 7, 2020 TRANSCRIPT of proceedings held on March 5, 2020 before Chief Judge Margaret M. Sweeney. Total No. of Pages: 1-77.

Release of Transcript Restriction set for 7/6/2020.

8) 13-698C Arrowood Indemnity Company . Preferred Direct*

April 6, 2020 Plaintiff’s think none of the Fairholme counts apply to their case

May 15, 2020 the court dismisses plaintiffs’ claims because it lacks jurisdiction to entertain their fiduciary duty and implied-in-fact-contract claims, and plaintiffs lack standing to pursue any of their claims. The court therefore GRANTS defendant’s motion to dismiss.

9) 14-740C Louise Rafter …………………………. Common Direct & Derivative*

March 31, 2020 plaintiff continue to stay until 21 days following resolution of Fairholme

10) 18-281C Owl Creek Asia I L.P………..………. Preferred, Direct *

11) 18-369C Akanthos Opportunity Master Fund .. Preferred, Direct *

12) 18-370C Appaloosa Investment ……………. Preferred, Direct *

13) 18-371C CSS LLC ……………………………………. Preferred, Direct *

14) 18-529C Mason Capital L.P………..………….. Preferred, Direct *

March 26, 2020 above 5 plaintiffs don’t want to give up the direct claims and doubt the counts in Fairholme properly represent their counts, and point out the law was breached

15) 18-1124C Wazee Street……………….………… Common, Class Action, Direct & Derivative

16) 18-1150C Highfields Capital………………….. Common & Preferred, Direct

17) 18-711C 683 Capital Partners………..……….. Common, Preferred, Direct

18) 18-712C Joseph S. Patt………………………..… Preferred, Direct

19) 18-1226C Perry Capital LLC……………………. Common & Preferred, Direct & Derivative

20) 18-1155C CRS Master Fund LP…..…………… Preferred, Direct

Above 6 Plaintiffs are staying

21) 18-1240C Quinn Opportunities Master LP … Preferred, Direct

May 19, 2020 – Status unknown

* Jones Days plaintiffs

Sisti v. Federal Housing Finance Agency

Case number: 17-005 (90-1762)(17-042)

Honorable: John James McConnell, Jr

District Court, D. Rhode Island

Claim: FHFA, Fannie Mae, and Freddie Mac are government entities

https://www.courtlistener.com/docket/6900150/sisti-v-federal-housing-finance-agency/

March 24, 2020 Stipulation ~Until – Set Scheduling Order Deadlines

The Parties report to the Court that they are currently re-engaged in negotiations aimed at resolving the action. In order to afford the Parties with sufficient time to complete these discussions and discovery (if necessary), the Parties jointly request the Court extend the scheduling order deadlines by three (3) months to the following:

Factual Discovery to close by 6/30/2020;

Plaintiff’s Expert Disclosures shall be made by 7/30/2020;

Defendants’ Expert Disclosures shall be made by 8/28/2020;

Expert Discovery to close by 9/30/2020; and

Dispositive Motions due by 10/30/2020.

https://www.courtlistener.com/recap/gov.uscourts.rid.41482/gov.uscourts.rid.41482.53.0.pdf

When decided FHFA, FNMA and FMCC are government entities for matters of constitutional claims of due process and will confirm or not the paragraph nobody can take action while in conservatorship.

https://ecf.rid.uscourts.gov/cgi-bin/show_public_doc?2017cv0005-39

Seila law v. Consumer Financial Protection bureau

***Decision in the last 2 weeks of June 2020***

Case number: 19-7 (17-56324)

Court: Supreme Court of the United States

Issues: (1) Whether the vesting of substantial executive authority in the Consumer Financial Protection Bureau, an independent agency led by a single director, violates the separation of powers; and (2) whether, if the Consumer Financial Protection Bureau is found unconstitutional on the basis of the separation of powers, 12 U.S.C. §5491(c)(3) can be severed from the Dodd-Frank Act.

https://www.scotusblog.com/case-files/cases/seila-law-llc-v-consumer-financial-protection-bureau/

Transcript of argument on Tuesday, March 3, 2020.

https://www.supremecourt.gov/oral_arguments/argument_transcripts/2019/19-7_j4ek.pdf

Audio: https://www.oyez.org/cases/2019/19-7

1) Questions asked by plaintiff: for cause violates the separation of powers

2) The Court added a second question: can for cause be severed from Dodd-Frank Act

Plaintiff and the government agree on the first question that “for cause” violates the constitution, but disagree on the second question

Plaintiff contends reverse the judgment and either decline to reach the question of severability or declare it is not severable.

The government argues that the Court should remand for further proceedings.

(The decision in this case will decide on Collins SCOTUS 19-422 “backward-looking relief” witch the 5th circuit en banc declined)

- 05/21/2020 – positive news from imfpub. Very positive for jps? not sure for commons?

Now that the Federal Housing Finance Agency has published a final capital rule of 4% for Fannie Mae and Freddie Mac, the next hurdle is cash-creation, namely just how quickly the two GSEs can build an estimated $250 billion they will need to escape the shackles of conservatorship…

Keep in mind, that since becoming wards of the federal government in September 2008, Fannie and Freddie received $191.4 billion in assistance from the U.S. Treasury, but then returned (since becoming mostly profitable again in 2012) roughly $301.1 billion. That comes out to a cash surplus of $109.7 billion for the two Congressionally chartered mortgage giants…

But will the assistance the two received from Treasury be officially forgiven as a way for the re-IPOs of Fannie and Freddie to move forward?…

According to one investor we know, “Treasury is expected to agree to use the overpayment it has already received (above the 10 percent original dividend rate) to count as some sort of prepaid asset.” Stay tuned…

- 05/20/2020 – initial analysis of the recap plan

ln order to get out of conservatorship we need a capital restoration plan that gets to $134 bil. After that, to get out from a consent decree, pay dividends and bonuses you’ll need another $99 billion.

$135B RBC + $99B Buffer to have no restrictions on dividends. At $160B, can pay 20% NI (~$4B, ~2.5%). They will want to hit this amount ASAP ($152B is minimum, too). If feasible, ~$100B equity offering.

HoldenWalker99 @HoldenWalker99

HoldenWalker99 @HoldenWalker99

- 05/20/2020 – New cap rule comes, it is 4% ($243 bil), which is higher than Mel Watt’s 3.25%. Will commons get crushed, and pref get big hair cut?

U.S. housing finance regulator unveils new capital framework for Fannie, Freddie

Re-proposed-Rule-on-Enterprise-Capital-5202020

FHFA Releases Re-Proposed Capital Rule for the Enterprises

FOR IMMEDIATE RELEASE, 5/20/2020

Mnuchin likes this plan

WASHINGTON – U.S. Treasury Secretary Steven T. Mnuchin issued the following statement today following the announcement of the Re-Proposed Capital Rule for the Enterprises by the Federal Housing Finance Agency:

“I commend Director Mark Calabria and the FHFA for their work on this issue. Establishing regulatory capital requirements for both GSEs represents an important step toward bringing the conservatorships to an end. Appropriate capitalization of the GSEs will be critical to protecting taxpayers, fostering market discipline, promoting stability in the housing finance system, and ensuring durable consumer access to mortgage credit.”

In addition, The new proposal is open to public comment, and the FHFA would like to finalize it by the end of 2020 so Fannie and Freddie could look to raise outside capital sometime in 2021, agency officials said.

- 05/20/2020 – so the capital plan is “very close” – from imfpubs

The worst kept secret in Washington this week: That the Federal Housing Finance Agency is close to releasing proposed capital requirements for Fannie Mae and Freddie Mac. How close? Very close, according to FHFA Director Mark Calabria, who spoke during a Mortgage Bankers Association forum Tuesday afternoon…

- 05/19/2020 – MC says the capital rule will come very soon. Be ready to buy.

- 05/18/2020 – get ready for the recap plan to come soon?

Fannie Mae to Issue Request for Proposals to Hire Financial Advisor

Announcement Represents Significant Milestone for the Company, Housing Finance System

Fannie Mae (OTCQB:FNMA) and Freddie Mac (OTCQB:FMCC) separately issue requests for proposals for hiring financial advisers that will facilitate their exit from government conservatorship.

Fannie said it’s seeking an underwriting financial adviser to “assist in developing and implementing a plan for recapitalizing and responsibly ending its conservatorship.”

Engaging a financial adviser is an important milestone in meeting Fannie’s 2020 FHFA scorecard objective to prepare a responsible transition plan for a potential exit from conservatorship, the company’s statement said.

Freddie said its adviser’s tasks would include assessing the company’s valuation, reviewing its business plan, identifying options for raising capital, and evaluating regulatory considerations during a transition period.

Fannie Mae and Freddie Mac head for the exit as COVID-19 rages

The GSEs announce they are looking for financial advisors in first step toward ending conservatorship

In the midst of the sharpest economic drop since the Great Depression, prompted by the COVID-19 pandemic, Fannie Mae and Freddie Mac said they are looking for financial advisors to underwrite what is likely to be the largest public share offering in U.S. history.

The timing of the announcement underscores the Trump administration’s determination to end the conservatorship of the world’s two largest mortgage financiers. The GSEs have to move quickly if they want to ensure they exit conservatorship before the November election, which could put a different administration in charge, said Jaret Seiberg, managing director of Cowen Group in Washington D.C.

It’s possible to hire financial advisors and handle the pandemic-induced turbulence in the housing market, said Fannie Mae CEO Hugh Frater. About 8% of U.S. mortgages are now in forbearance after borrowers lost jobs because of COVID-19 shutdowns, according to the Mortgage Bankers Association.

- 05/11/2020 – FNMAS jumps more than 8% today. The following speculations might have something right

Fnma trader

May 4

I dumped common and bought more prefs today – nothing that new except the accounting standards adoption but some dreams below:

1. change in GSE accounting standards – more conservative thus less retained earnings. Thus made me think that commons will be cheaper and prefs will likely convert into more commons.

2. Covid plus accounting standards from hell are not causing the gse’s to take losses so the capital rule could be less conservative than the old one as the players are not as motivated to keep the GSEs captive.

3. Given the reduced earnings , the financial advisors likely could be talking to heavyweight firms that provide a faster exit from conservatorship than a regular public secondary offering post a year or two of crappy earnings thus making them cheaper and thus more interesting to a large buyer. You’d buy the prefs if you were getting pitched? You might buy common first but the warrants and conversion would scare you

4. Berkshire is one of the firms talking to the advisors? Buffett always wants to buy something big at a great price when the market is in pain…. he must be spending time on this now and he knows the prefs and capital structure well. He’d need massive legal assurance of course and might only want one combined entity ?

5 imminent capital rule?

6. Supreme Court CFPB ruling

When S does well, the $50s follow dutifully behind…

- 04/30/2020 – read it in details tomorrow

Fannie Mae and Freddie Mac are ready for recession

- 04/22/2020 – Charles Gasparino said the 2021 timetable might extend again